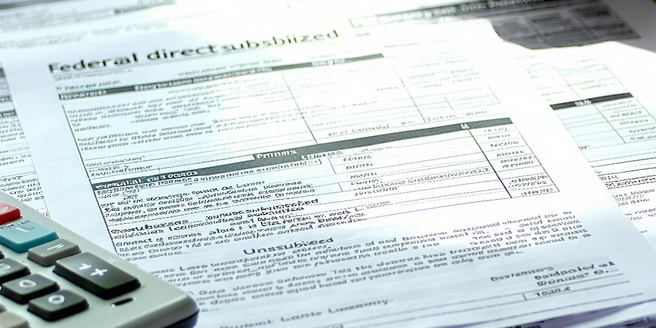

Understanding Your Loan Types

| Loan Type | Interest Rate | Repayment Term |

| Federal Direct Subsidized | Fixed | 10-25 years |

| Federal Direct Unsubsidized | Fixed | 10-25 years |

| Federal PLUS Loan | Fixed | 10-25 years |

| Private Loans | Variable or Fixed | Varies |

| Parent PLUS Loan | Fixed | Up to 25 years |

Repayment Plan Strategy

Creating a repayment plan that fits your financial situation is essential for managing your student loan debt effectively. Start by reviewing your current loans and understanding the terms and conditions associated with them. Consider consolidating loans if it simplifies management while offering a better interest rate. Prioritize loans with higher interest rates to repay them faster, reducing overall financial burden. It is crucial to set a realistic budget that accommodates regular payments. Utilize tools like loan calculators to foresee long-term impacts of your strategy. Ensure you revisit your strategy periodically for potential optimizations. Regular payments are crucial to maintain a good credit standing, which can impact future financial ventures. Being proactive in managing your loans can help mitigate stress and keep your financial health on track.

Federal Loan Repayment Options

Federal student loans offer a variety of repayment plans to meet different borrower needs. Standard repayment plans ensure loans are paid off within 10 years of monthly slated payments. Graduated repayment plans start with lower amounts that increase over time, aligning with expected income growth. Extended repayment offering allows up to 25 years’ pay off time, with either fixed or graduated amounts. Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE) depend on discretionary income, adjusting payments accordingly. Additionally, consolidation loans could make debt more manageable, although sometimes increasing interest or extending repayment duration. Being knowledgeable about these options is the key to making informed decisions about your loan repayment strategy.

Income-Driven Repayment Plans

Income-driven repayment plans provide an alternative to standard or graduated repayment schemes, offering flexibility to borrowers by tailoring monthly payment amounts to specific income levels. These plans—Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE)—allow payment adjustments according to discretionary income while potentially extending the loan term. Payments are recalculated annually to reflect any changes in income or family size, ensuring affordability. While these plans offer lower monthly payments, they may result in higher overall loan costs due to interest accumulation. Furthermore, any loan balance that remains after 20-25 years may qualify for forgiveness, although it may be subject to taxation. Borrowers should carefully consider their long-term financial stability before committing to these plans.

Benefits of Loan Consolidation

Loan consolidation merges multiple loans into a single payment, simplifying repayment and potentially lowering monthly costs. Many individuals find this process beneficial in managing their debt more effectively. Consolidation can extend loan term—up to 30 years—resulting in smaller monthly payments, easing immediate financial pressure. Fixed interest rates offer predictability, protecting against future rate hikes. Federal Direct Consolidation loans grant access to additional repayment plans like Income-Driven Repayment, increasing flexibility based on financial conditions. However, by prolonging repayment, total interest may increase compared to repaying loans separately. It’s crucial to weigh short-term affordability against long-term expense, considering whether consolidation aligns with your goals. Evaluating interest rates, repayment terms, and eligibility for forgiveness programs can aid in determining if consolidation suits your circumstances.

Pros and Cons of Refinancing

Refinancing student loans can offer advantages, such as securing a lower interest rate which reduces overall interest payments and allows faster debt clearance. Additionally, consolidating into one loan simplifies the repayment process. Depending on the lender, borrowers might be able to select favorable terms tailored to individual financial situations. However, refinancing, particularly with private lenders, may negate benefits associated with federal loans, such as forbearance options and eligibility for forgiveness programs. Furthermore, the interest rate offered depends on credit history—those with limited or poor credit may not benefit. Consideration of both personal financial goals and the potential loss of federal protections are essential when deciding on refinancing options. Determining whether it is a personal fit is crucial in the decision-making process.

Deferment and Forbearance Options

Deferment and forbearance temporarily suspend loan payments, providing relief in situations like financial hardship or pursuing higher education. During deferment, no interest accrues on subsidized federal loans, preserving loan balance during postponement. Forbearance allows for temporary suspension or reduction of payments but often results in interest continuing to accrue, which can increase the loan balance over time. Both options ensure loan accounts remain in good standing during periods of financial difficulty but ideally should be utilized as short-term solutions, given the potential for increased total loan costs. Borrowers should evaluate these options carefully, ensuring other strategies have been exhausted and the potential financial impact understood. Seeking advice from loan servicers can aid in making informed decisions.

Loan Forgiveness Programs to Explore

Loan forgiveness programs offer significant relief by forgiving remaining debt after a certain number of qualifying payments. Public Service Loan Forgiveness (PSLF) is available to those in nonprofit or government positions making 120 qualifying payments under eligible repayment plans. Teacher Loan Forgiveness rewards educators teaching low-income schools with up to $17,500 forgiveness. Income-driven plans provide forgiveness of remaining balances after 20 or 25 years of consistent payments, though this may be taxable. Engaging with these programs requires careful employment and repayment tracking to meet eligibility criteria. They offer significant financial benefits to those who meet specific requirements. Borrowers should thoroughly research the specifics of each program, ensuring their ability to fully capitalize on potential forgiveness benefits.

Tips for Making Extra Payments

Making additional payments on student loans can substantially reduce total loan costs by decreasing principal amounts and interest expenses. Prioritize higher interest loans for any surplus payments, maximizing financial efficiency. Consider scheduling extra payments early in the repayment cycle when the impact on principal is greatest. Utilizing windfalls such as tax refunds or bonuses for additional payments can accelerate debt reduction without straining monthly budget allocations. Ensure servicers apply extra payments specifically to the principal, preventing unnecessary interest costs. While such strategies don’t immediately reduce required payments, they significantly shorten the repayment period and decrease total interest paid over the loan’s life. Careful attention to both budgetary constraints and explicit payment instructions ensures extra payments effectively contribute to financial health.

Common Mistakes to Avoid in Repayment

Blindly selecting repayment plans without thorough research often results in suboptimal choices that fail to match individual financial situations. Many borrowers overlook the importance of personalized financial planning when choosing repayment options. Failure to understand interest rate terms can result in unexpected costs—it’s crucial to evaluate fixed versus variable options. Ignoring income changes can lead to misaligned repayment strategies; borrowers should consistently reassess financial standing. Overlooking benefits of automatic payment discounts—often around 0.25%—is a forgone saving opportunity. Neglecting emergency funds and assuming loan forgiveness programs don’t require thorough understanding can be financially detrimental. Proactively managing repayments requires awareness of available options and potential pitfalls. Consistent financial evaluation aligns repayment plans to changing circumstances, helping to avoid unnecessary costs and stress.